The Dow Jones Industrial Average and S&P 500 ended Wednesday’s session with minimal changes as momentum from the postelection rally began to wane. Despite early gains, investor sentiment cooled as attention turned to key inflation data that met expectations, signalling potential implications for the Federal Reserve’s next policy moves. The S&P 500 edged up, while the Dow also rose. Meanwhile, the Nasdaq Composite dipped, weighed down by tech stocks, as investors digested inflationary signals that could shape rate cut prospects in December.

Key Takeaways:

- Dow and S&P 500 Close Near Flatline: The Dow Jones Industrial Average managed a modest gain on Wednesday, adding 47.21 points, or 0.11%, to close at 43,958.19. The blue-chip index had surged by as much as 230 points earlier in the session before losing steam, reflecting the fading momentum of the postelection rally. The S&P 500 also showed little movement, edging up only 0.02% to end the day at 5,985.38.

- Nasdaq Slips as Tech Sector Lags: The Nasdaq Composite faced a decline on Wednesday, slipping 0.26% to close at 19,230.74. This decline followed a day when the Nasdaq had shown resilience, but the faltering postelection rally and inflation concerns pushed it back into negative territory.

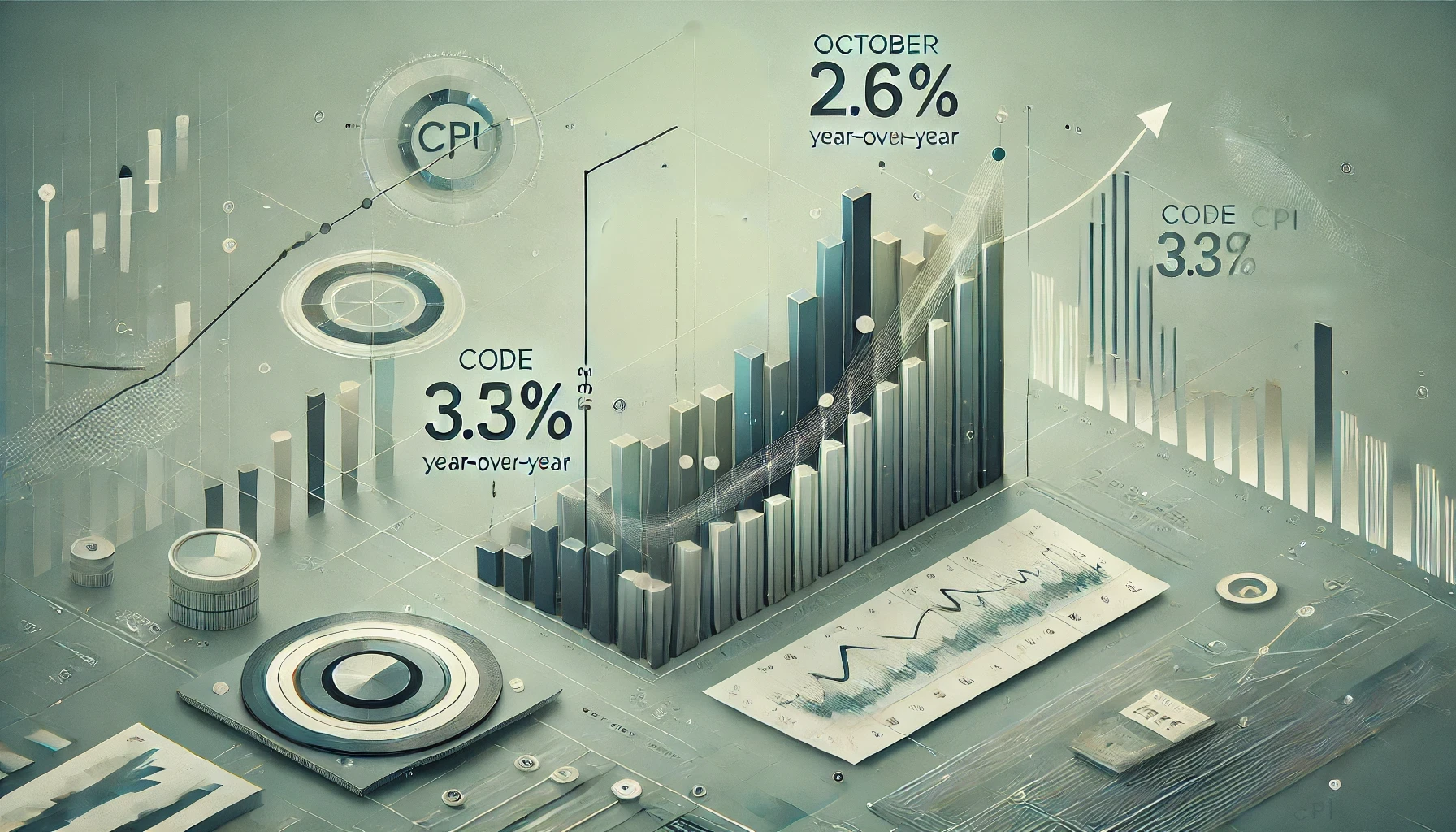

- Inflation Data Aligns with Expectations, Raising Rate Cut Prospects: October’s consumer price index (CPI) climbed to an annual rate of 2.6%, precisely in line with economists’ predictions, offering a mild yet steady increase in inflation. The core CPI, which excludes food and energy, also met expectations with a 3.3% rise year-over-year.

- Bitcoin Surges to New High Amid Postelection Rally: Bitcoin surged to an all-time high on Wednesday, briefly surpassing $93,000 before settling at $91,201.09, marking a gain of over 1% for the day. The cryptocurrency reached an intraday peak of $93,469.08, supported by optimism from the postelection rally. However, other cryptocurrencies saw profit-taking, with Ether and XRP declining, as traders balanced gains across the digital asset landscape.

- European Markets Dip as Traders Digest US Inflation Data: European stocks closed lower on Wednesday, with the pan-European Stoxx 600 index shedding 0.17%. Tech stocks across Europe were down 1.2%, contributing to the index’s losses. The FTSE 100 managed a slight gain, rising 0.06% to close at 8,030.33, while France’s CAC 40 fell to its lowest level in over three months, closing around 7,200 after dropping 0.14%. In Germany, the DAX index slipped 0.16% following the latest US inflation report, which met expectations but cast a shadow over global markets. Notably, Just Eat Takeaway and Siemens Energy defied the trend, soaring 15.95% and 19%, respectively, on strong corporate developments.

- Asia-Pacific Markets Slide as Rally Settles Down: The postelection rally from Wall Street failed to carry over to Asia, where major indices largely fell. Japan’s Nikkei 225 dropped 1.66% to close at 38,721.66, while the Topix index declined 1.21% to 2,708.42. In South Korea, the Kospi fell sharply by 2.64%, ending at 2,417.08, with the Kosdaq Index sliding 2.94% to 689.65. Australia’s S&P/ASX 200 also declined, finishing 0.75% lower at 8,193.4. In contrast, China’s CSI 300 rose 0.62%, closing at 4,110.89, with hopes for policy support buoying sentiment, even as the broader regional market faced pressure.

- Oil Rebounds Amid Short-Covering Despite OPEC’s Gloomy Demand Outlook: Oil prices bounced back on Wednesday, with Brent crude futures rising 39 cents, or 0.54%, to settle at $72.28 per barrel. US West Texas Intermediate crude futures also gained, closing up 31 cents, or 0.46%, at $68.43. This recovery followed a period of selling pressure, driven by OPEC’s downward revision of its global demand forecast for 2024 and 2025 due to weakness in China and other regions. Despite the rebound, the market remains cautious, with attention turning to the upcoming International Energy Agency demand forecast update.

- 10-Year Treasury Yield Holds Steady After Inflation Report Meets Expectations: The yield on the 10-year US Treasury remained largely unchanged on Wednesday, rising less than 2 basis points to 4.451% as investors evaluated the implications of October’s inflation data. The 2-year Treasury yield fell about 7 basis points to 4.275%. This subdued inflation reading keeps the Federal Reserve on track for a likely interest rate cut in December, with the market last showing a 79% likelihood of a quarter-percentage-point reduction according to the CME FedWatch Tool.

FX Today:

- EUR/USD Faces Persistent Pressure Below Resistance Levels: The EUR/USD pair concluded at 1.0563, maintaining a bearish outlook as it struggled to move above key resistance points. During the day, attempts to gain traction were met with strong selling pressure around the 50-period Simple Moving Average (SMA) at 1.0750, preventing any sustained rally. This consistent rejection highlights the sellers’ control, with the pair also trading under the 100-period SMA at 1.0786 and the 200-period SMA at 1.0873, signalling a challenging path forward for any potential bullish recovery. If the pair declines further, support may be found near the 1.0500 level. Should EUR/USD manage to break above the 50-period SMA, it could signal a shift in momentum, although additional hurdles lie at the 100-period and 200-period SMAs.

- GBP/USD Extends Decline Amid Downward Momentum: GBP/USD settled at 1.2709, continuing its downward path as it encountered resistance near the 50-period SMA at 1.2898. Buyers made efforts to push the price higher, but the strong selling interest at this level allowed the bearish trend to persist. With the pair remaining below the 100-period SMA at 1.2930 and the 200-period SMA at 1.3025, the pressure remains on the downside. Should the decline continue, GBP/USD may find support near 1.2650, where buyers might step in. A break above the 50-period SMA could indicate a temporary recovery, though further resistance would likely limit any upward movement.

- USD/CHF Shows Strength as Buyers Hold Above Moving Averages: USD/CHF closed at 0.8859, displaying a resilient bullish stance as it maintained levels above significant support. Earlier, the pair briefly dipped towards the 50-period SMA at 0.8738 and the 100-period SMA at 0.8700, where buyers regained control, driving the pair upwards. With the USD/CHF trading above the 200-period SMA at 0.8634, the positive sentiment remains intact. If the pair continues its ascent, resistance may be found near the 0.8900 level, where sellers could re-enter. However, a retreat below the 200-period SMA would indicate a potential weakening of the bullish trend.

- Gold Slides as Resistance at Moving Averages Holds Firm: Gold closed lower at $2,576.28 after attempting to push past critical resistance levels earlier in the day. The metal faced strong resistance around the 50-period SMA at $2,677.33 and the 100-period SMA at $2,713.17, which held firm, leading to a reversal. The drop below the 200-period SMA further confirmed the bearish outlook, with potential support at $2,560.00, a key level for buyers to defend against further losses. A recovery above the 50-period SMA could indicate renewed bullish interest, though significant resistance would likely persist around the 100-period SMA at $2,713.17.

Market Movers:

- Charter Communications Rises on Liberty Broadband Acquisition: Charter Communications shares rose 3.6% after announcing an all-stock acquisition of Liberty Broadband. Liberty Broadband, however, saw its stock fall by about 5% as investors evaluated the transaction’s impact on its valuation. The deal strengthens Charter’s position in the cable industry.

- Rocket Lab Soars on Revenue Beat and New Customer Deal: Rocket Lab shares surged 28.4% after reporting third-quarter revenue of $104.8 million, up 55% from the previous year and above expectations. The company also secured its first customer for its Neutron vehicle, boosting its growth outlook.

- Maplebear Declines on Weak Fourth-Quarter Guidance: Maplebear, parent of Instacart, saw an 11% drop in shares after its fourth-quarter guidance fell below analysts’ expectations, despite beating third-quarter estimates. The cautious outlook raised concerns over future growth in the competitive grocery delivery market.

- Spotify Jumps on Positive Profit Forecast: Spotify’s stock rose 11.4% as it issued a better-than-expected fourth-quarter profit forecast, despite missing third-quarter earnings expectations. Monthly active users reached 640 million, slightly surpassing forecasts and boosting investor confidence.

- Rivian Rallies on Volkswagen Partnership News: Rivian shares gained 13.7% after announcing a $5.8 billion joint venture with Volkswagen, which could see Volkswagen using Rivian’s software and architecture in future EV models. The partnership enhances Rivian’s position in the EV market.

- SoundHound AI Drops on Revenue Guidance Miss: SoundHound AI fell 17.1% after providing 2024 revenue guidance below expectations, ranging between $82 million and $85 million. The third-quarter adjusted loss was smaller than anticipated, but the lower forecast disappointed investors.

- Spirit Airlines Plummets Amid Bankruptcy Fears: Spirit Airlines shares dropped over 59% following reports that it may file for bankruptcy within weeks after failed merger talks with Frontier. The uncertainty around Spirit’s financial stability spurred a wave of selling.

As Wednesday’s session came to a close, markets displayed mixed sentiments amid inflation concerns and waning postelection momentum. The Dow and S&P 500 held near flat, reflecting cautious optimism as traders digested inflation data that aligned with expectations and increased hopes for a December rate cut. While the Nasdaq slipped, driven by a pullback in tech stocks, Bitcoin surged to record highs, benefiting from postelection gains. Meanwhile, European and Asia-Pacific markets largely retreated, mirroring US sentiment, with declines in key indices and sectors. Oil prices saw a modest rebound on short-covering, and gold faced downward pressure as sellers regained control. Investors now turn their attention to upcoming economic indicators, with inflation and labour market data likely to influence market direction in the days ahead.